The 41% decline in Wireline Networks revenues in 2002 compared to 2001 was primarily due to a substantial reduction in capital spending by

our service provider customers.

The considerable decline in the circuit and packet voice portion of this segment was the result of continued reduced demand in the local

exchange and interexchange carrier markets due to the significant industry adjustment, including industry consolidation and tightened capital

markets, and the substantial decline in demand for traditional circuit switching products. During 2002, many of our service provider customers

continued to delay their investment decisions on our packet voice solutions due to the technology evolution uncertainty in the industry. In

2002, we continued to experience significant pricing pressures on our traditional circuit switching products due to the increased competition for

service provider customers.

The considerable decline in revenues in the data networking and security portion of this segment was primarily due to a decline in demand for

mature products, compounded by the ongoing industry adjustment as our service provider customers, in all regions, continued to reduce their

capital expenditures.

From a geographic perspective, the 41% decline in Wireline Networks revenues in 2002 compared to 2001 was primarily due to a 41% decline

in the U.S., a 32% decline in EMEA, a 57% decline in CALA, and a 39% decline in Asia Pacific. The declines in all regions were primarily

attributable to the substantial reduction in spending by our service provider customers as a result of the factors mentioned above.

In 2004, our service provider customers continued to increase the deployment of packet-based technologies in their communications networks

as they looked for ways to optimize their existing networks and offer new revenue generating services while limiting capital expenditures and

operating costs. However, the timing of when service provider customers will deploy packet-based technologies on a wider scale is still

unclear. Further, it is difficult to determine the effect the FCC decision regarding the regulation of the availability of UNEs and subsequent

adoption on December 15, 2004 of new unbundling rules in response to the remand by the U.S. Court of Appeals for the D.C. Circuit will have

on our business. The demand for our traditional circuit switching products has continued to decline as certain service providers continued to

reduce their capital expenditures on these legacy technologies. While we have seen encouraging indicators in certain areas of the wireline

service provider market, we can provide no assurance that the growth areas that have begun to emerge will continue in the future.

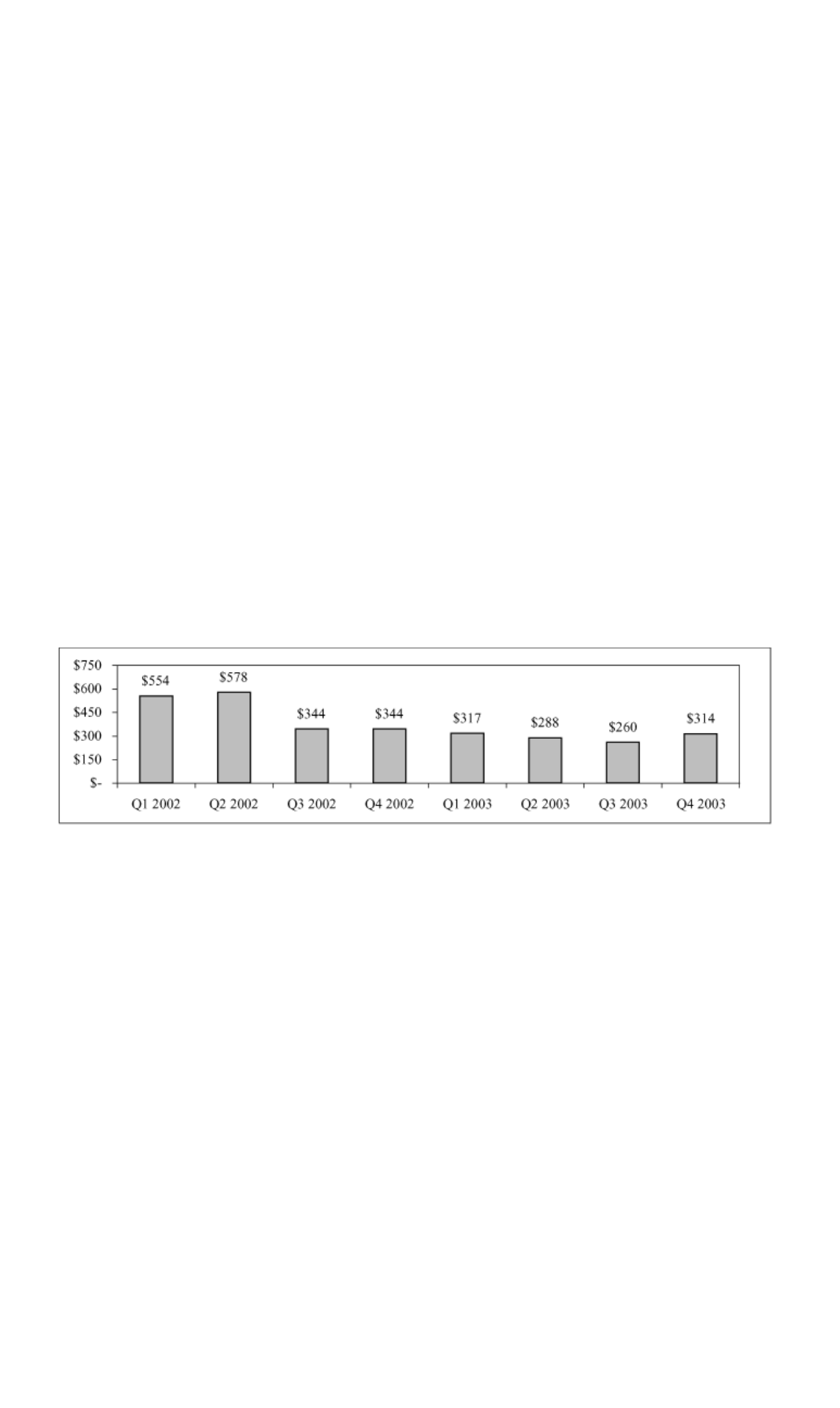

Optical Networks revenues

The following chart summarizes recent quarterly revenues for Optical Networks:

Optical Networks revenues declined 35% in 2003 compared to 2002. The decline was primarily the result of the continuing industry

adjustment, excess capacity, tightened capital markets mainly during the first half of 2003 and reductions in capital spending by our EMEA,

U.S. and Canada customers in both the long-haul and metro optical portions of this segment.

Revenues in the long-haul portion of this segment declined substantially in 2003 compared to 2002. The substantial decline was primarily due

to the continuing industry adjustment, excess capacity, tightened capital markets mainly during the first

61

2002 vs. 2001

2004 and 2005

2003 vs. 2002