The period of relative industry stability that had characterized the second half of 2003 continued into 2004. For 2005, we expect revenue

growth over 2004 primarily due to continued growth in the above areas.

Spending in these areas of our business has been partially offset by customers limiting their investment in mature technologies as they focus on

maximizing return on investment capital. In addition, we have continued to experience pricing pressures on sales of certain of our products as a

result of increased competition particularly from low cost suppliers. Further, while customer support generally remains strong, we believe the

ongoing restatement activities and the internal restructuring and realignment programs initiated in August 2004 have adversely impacted

business performance in 2004.

Consolidated revenues for the third and fourth quarters of 2004 reflect certain of these trends, with third quarter 2004 consolidated revenues

lower than previously announced preliminary unaudited consolidated revenues for the second quarter of 2004. Our fourth quarter is expected to

be our strongest quarter in 2004. Our quarterly results of operations will not necessarily be consistent with our historical quarterly profile or

indicative of our expected results in future quarters. See “Risk factors/forward looking statements” for other factors that may affect our

revenues.

Wireless Networks revenues

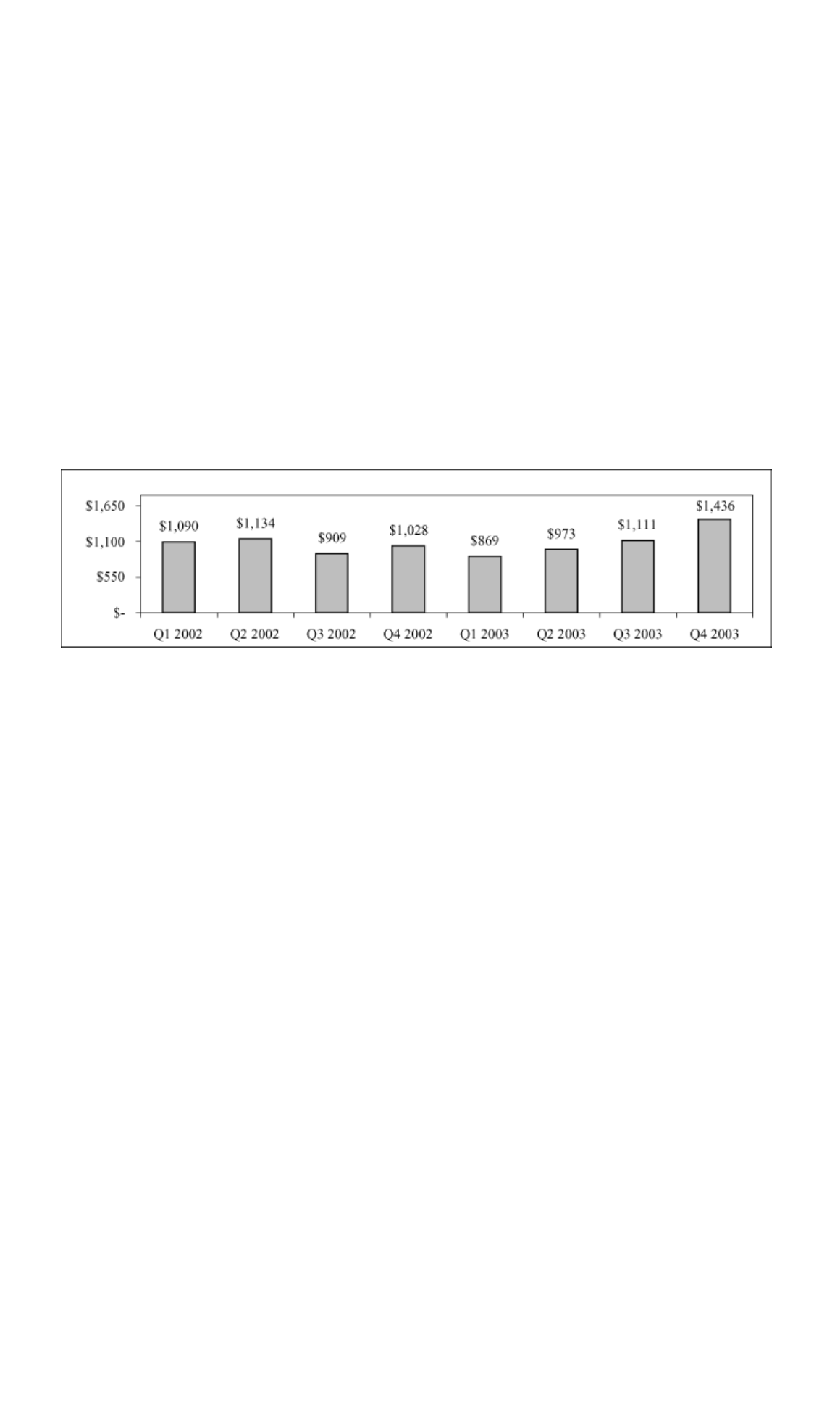

The following chart summarizes recent quarterly revenues for Wireless Networks:

Wireless Networks revenues increased 5% in 2003 compared to 2002 due to a 31% increase in the second half of 2003 partially offset by a

17% decrease in the first half of 2003 compared to the same periods in 2002. The 31% increase in the second half of 2003 was primarily due to

increased spending by our wireless service provider customers on our GSM, CDMA and UMTS technologies as a result of new contracts with

certain customers and other customers expanding their existing networks to meet increased subscriber demand. The 17% decline in the first

half of 2003 was primarily due to the ongoing focus by wireless service providers on capital and cash flow management and increased

competition for customers by wireless service providers. As a result, many of our customers heavily scrutinized their capital expenditure

requirements and postponed or reduced their capital spending during the first six months of 2003.

CDMA revenues increased in 2003 compared to 2002 due to a substantial increase in revenues in the second half of 2003 compared to the

same period in 2002. This substantial increase was partially offset by a decrease in the first half of 2003 compared to the same period in 2002.

The substantial increase in CDMA revenues in the second half of 2003 compared to the same period in 2002 was primarily due to a substantial

increase in the U.S. and Canada as a result of our customers expanding their existing networks and upgrading their existing networks to higher

data speeds. The substantial increase in the U.S. and Canada was partially offset by a substantial decrease in EMEA. This substantial decline

was primarily due to the completion of key customer network deployments during the first half of 2003, which had been underway in 2002.

The decrease in CDMA revenues in the first half of 2003 compared to the same period in 2002 was primarily due to a

56

• voice over packet technologies;

• third generation wireless technologies; and

• expansion and enhancement of existing networks due to subscriber growth and competitive pressures.

2003 vs. 2002